Gold investment plans are woven into the Indian money mindset, not just the balance sheet. From the first gold bangle gifted at birth to the jewellery passed down at weddings, gold quietly becomes every family’s first “investment”, long before they hear terms like equity or mutual fund.

This deep cultural comfort is exactly why structured gold investment plans work so well in India, they turn an age old habit into a disciplined wealth-building strategy. Instead of impulsively buying jewellery, investors can use gold saving plans to accumulate gold systematically for future goals like children’s marriage or financial security1.

On the portfolio side, gold is more than sentiment; it is a powerful diversification asset. Because gold often behaves differently from stocks and bonds, allocating a portion of your portfolio to a gold investment plan can smooth out volatility and protect your overall wealth during market stress. Ready to explore the full spectrum. Dive into the different types of gold investment plans in India next, from timeless physical gold to cutting-edge digital options.

Different Types Of Gold Investment Plans In India

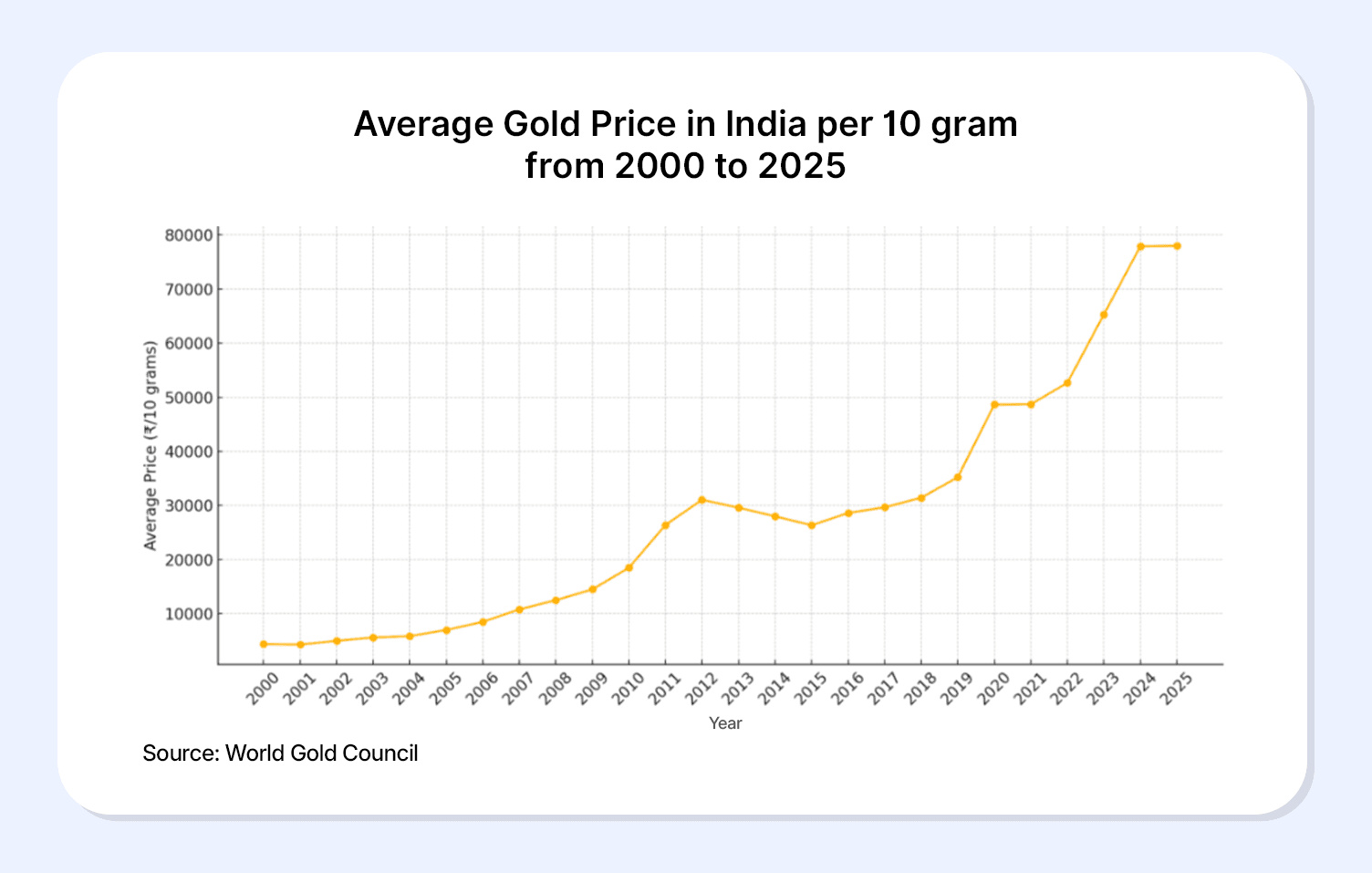

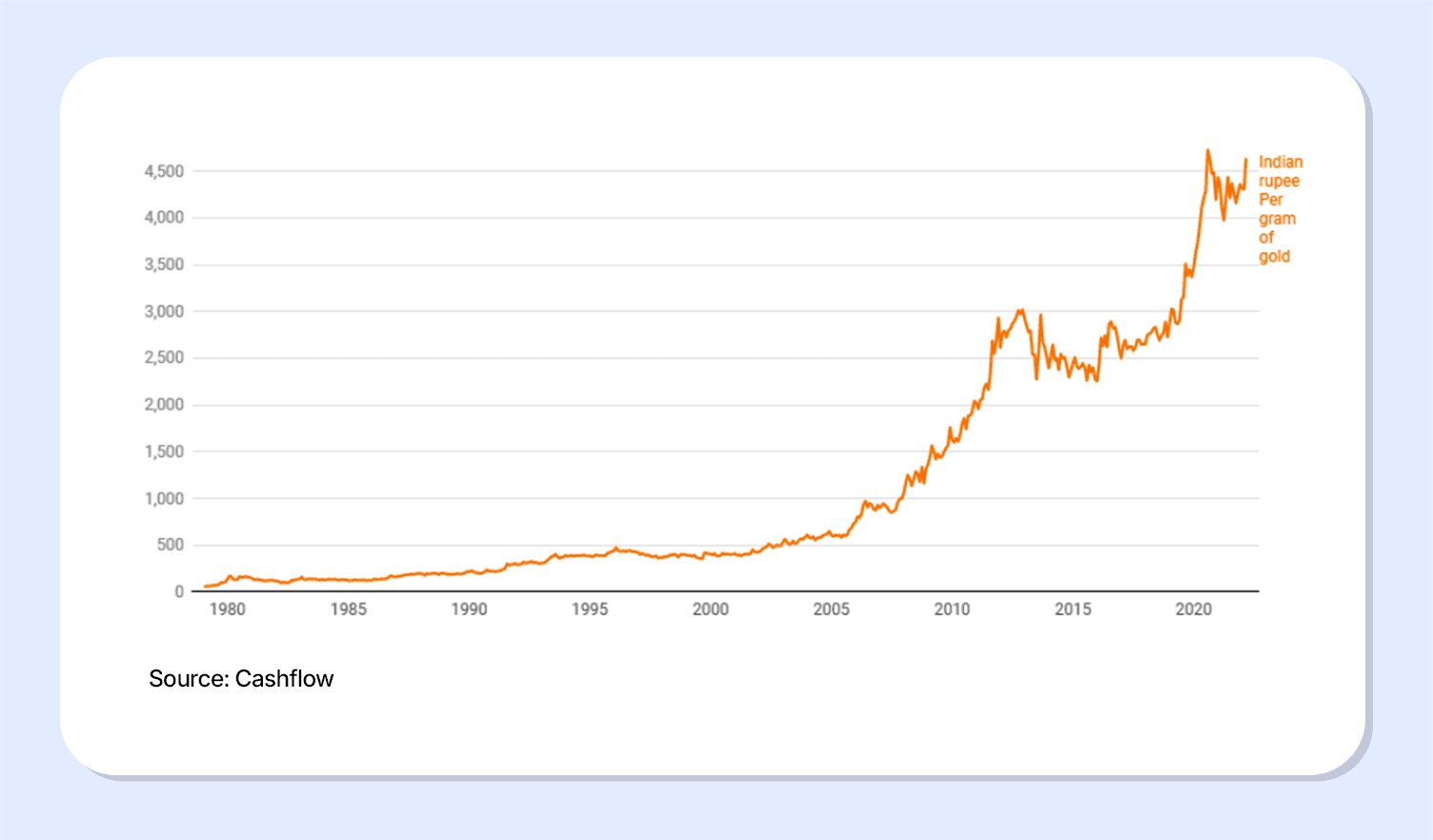

Indian investors today can choose from a wide spectrum of gold investment plans, ranging from traditional jewellery to fully digital, paperless products. This evolution matters because Indian households collectively hold an estimated 25,000–34,600 tonnes of gold, valued at roughly 80–120% of India’s GDP, making gold a system level savings instrument, not just a lifestyle choice.

1. Physical gold plans

Physical gold includes jewellery, coins, and bars bought through jewellers and banks, often supported by jeweller gold saving schemes where investors deposit monthly for 10–12 months and redeem in gold at the end. While this suits cultural and ceremonial needs, investors pay making charges of 5–25% on jewellery and bear storage and security risks, which can significantly reduce effective returns over time.

2. Gold ETFs and gold mutual funds

Gold ETFs invest in 99.5% purity bullion and trade on stock exchanges, typically tracking domestic gold prices with low tracking error. In FY24, gold ETFs in India delivered average returns of around 21–22% and attracted inflows of about INR 7,367 crore, reflecting strong investor interest in market linked gold exposure. Gold mutual funds (fund of funds) route money into these ETFs, allowing investors without demat accounts to access the same asset class via SIPs3.

3. Sovereign Gold Bonds (SGBs)

SGBs are RBI issued government securities denominated in grams of gold with an 8 year maturity and an exit option from year 5. They pay 2.5% interest per annum on the issue price, semi annually, and capital gains on redemption at maturity are fully tax exempt, making them one of the most return efficient gold investment plans for long term holders. As of recent estimates, over INR 64,000 crore has been invested in SGBs, underlining rising preference for this paper gold format4.

4. Digital gold plans

Digital gold lets investors buy fractional gold online, often starting from as low as INR 1, backed by 24K stored in insured vaults. It is popular for micro savings and daily SIP style investing, but investors must scrutinise provider regulation, storage terms, and buy–sell spreads because digital gold currently has no dedicated f

| Parameter | Physical gold | Gold ETF | Gold mutual fund | Sovereign Gold Bond | Digital gold |

| Typical purity (karat or %) | 22 | 24 | 24 | 24 | 24 |

| Making / product charge range (%) | 5–25 | 0–1 | 0–2 | 0 | 1–3 |

| Storage / platform cost p.a. (%) | 0–1 | 0.1–0.5 | 0.5–1.5 | 0 | 0–0.5 |

| Average 1 year return FY24 (%) | ~18–20 | ~21–22 | ~20–22 | ~22–25 | ~20–22 |

| Interest / yield over gold price (%) | 0 | 0 | 0 | 2.5 | 0 |

| Recommended minimum holding period (years) | 5+ | 1+ | 3+ | 5 | 0.5+ |

| Tenure / maturity (years) | Unlimited | Unlimited | Unlimited | 8 | Unlimited |

| Exit penalty / liquidity constraint (1–5)* | 2 | 1 | 2 | 4 | 2 |

| Regulatory / counterparty risk (1–5)** | 3 | 2 | 2 | 1 | 4 |

Source: Cleartax5

1 = very liquid, 5 = most constrained, 1 = lowest risk (sovereign), 5 = highest provider risk.

Understanding these options sets the stage for exploring the specific benefits of investing through structured gold plans in the next section

Benefits Of Investing Through Gold Plans

Structured gold investment plans offer compelling advantages over traditional physical gold buying, especially in convenience, safety, and accessibility for modern investors. These benefits make gold a more practical portfolio tool, particularly when Indian households already hold 25,000–34,600 tonnes of gold worth $3.8–5 trillion.

1. Convenience and liquidity

Gold ETFs and mutual funds trade on stock exchanges or via apps, enabling instant buying and selling without visiting a jeweller—ETFs saw INR 7,367 crore inflows in FY24 alone. Digital gold platforms allow 24/7 transactions and SIPs starting at INR 1–INR 10, turning impulsive purchases into disciplined saving habits. SGBs, while less liquid with a 5-year lock-in, still offer secondary market trading and premature redemption from year 57.

2. Lower storage risk

Unlike physical gold, which exposes investors to theft, loss, or damage (requiring lockers at 0.5–1.5% annual cost), paper gold options like ETFs, mutual funds, SGBs, and digital gold store assets professionally in insured vaults at minimal or zero extra cost. This eliminates the 3–4% of household gold reportedly idle due to storage concerns, freeing up mental and financial bandwidth.

3. Smaller ticket sizes

Structured plans democratise gold investing: Gold mutual funds accept SIPs from INR 100, digital gold from INR 1, and SGBs from 1 gram (INR 7,000–8,000 at current rates). This suits young professionals and salaried individuals building wealth gradually, unlike physical gold’s higher upfront commitment often tied to occasions8.

4. Risk–return comparison

Gold plans generally deliver superior net returns due to lower costs: SGBs offer gold price upside plus 2.5% fixed interest (tax-free at maturity), outperforming physical gold’s ~18–20% FY24 return after charges. ETFs matched ~21–22% with high liquidity, while digital gold adds leasing income potential of 3–4% but carries higher counterparty risk. A risk–return graph would show SGBs clustering high on both axes (low risk, high return via interest), ETFs balancing medium risk with liquidity, and physical/digital at higher risk ends.

Risk-Return Snapshot (FY24 indicative)

| Option | Net Return (%) | Risk Score (1-5) | Fixed Yield | Liquidity Rank |

| Physical Gold | ~18–20 | 3 | 0% | Medium |

| Gold ETF | ~21–22 | 2 | 0% | High |

| Gold Mutual Fund | ~20–22 | 2 | 0% | Medium |

| SGB | ~22–25 | 1 | 2.5% | Low (5-yr) |

| Digital Gold | ~20–22 | 4 | 0–4% | High |

These benefits position gold plans as essential for diversification, hedging inflation, and liquidity in volatile times. With these benefits clear, the next section explores how to choose the right gold investment plan based on your goals, horizon, and risk profile.

How To Choose The Right Gold Investment Plan

Picking the perfect gold investment plan transforms gold from a cultural keepsake into a smart financial weapon. Your choice among gold investment options India hinges on three game-changers: investment horizon, liquidity needs, and tax efficiency.

Long horizon (5+ years) Sovereign Gold Bonds shine with 2.5% fixed interest plus tax-free maturity gains—ideal for retirement or child’s wedding via disciplined gold saving plans. Short-term tactical plays suit Gold ETFs for quick market-linked exposure without locker hassles.

Liquidity crunch ETFs and digital gold let you invest in gold India instantly via apps—ETFs trade like stocks, digital starts at INR 1. SGBs lock funds until year 5 (though secondary markets exist), while physical gold means jeweller negotiations and purity worries.

Tax smart SGBs win big—capital gains exempt at maturity, interest taxable but overall superior to ETFs’ 12.5% LTCG post-indexation. Physical gold triggers 20% LTCG plus STT hassles. Digital gold follows VDA tax (30%), making it costlier for flips.

Match your goal: SGBs for steady compounders, ETFs for active traders, digital for micro-savers. Gold saving plans via SIPs in mutual funds bridge convenience and discipline. Skip emotional jewellery buys—choose data-driven gold that grows your wealth, not just your locker9.

Conclusion

Gold remains India’s unbeatable wealth guardian, evolving from locker treasures to smart gold investment plans that supercharge your portfolio. We have decoded options—physical for tradition, SGBs with 2.5% interest and tax perks, ETFs surging INR 7,367 crore in FY24, mutual funds for SIP ease, and digital from INR 1—amid 25,000+ tonnes household holdings worth trillions.

Benefits Lightning convenience, zero theft risks, micro-entry for all budgets, and superior net returns like SGBs’ ~22–25% FY24 haul. Match your play: long-haul SGBs, liquid ETFs, or starter digital gold saving plans.

Platforms like Grip Invest elevate this, SEBI-regulated for high-yield bonds and FDs (up to 14% p.a.), they pair seamlessly with gold for diversified, stable growth from just INR 1,000, minus physical gold’s hassles. Ditch emotional buys. Build legacy wealth with data-driven gold that hedges inflation and compounds quietly. Your future self will thank the savvy choice.

FAQs

1. Which gold investment plan is best in India?

No single winner—SGBs top for long-term (5+ years) with 2.5% interest and tax-free gains; ETFs shine for liquidity and ~21–22% FY24 returns; digital gold suits micro-SIPs from INR 1.

2. Are gold investment plans safe?

Highly safe overall: SGBs carry sovereign guarantee (risk score 1/5), ETFs via regulated exchanges (2/5), while digital gold needs provider scrutiny (4/5). All beat physical gold’s theft risks.

3. Is gold better than FD or bonds?

Gold hedges inflation better (unlike FDs at 6–7%), complements bonds for diversification—Grip Invest pairs high-yield FDs (up to 14%) with gold for balanced alpha. Use gold for 5–10% portfolio allocation, not core fixed income.

References:

1. Bank of Baroda, accessed from https://bankofbaroda.bank.in/banking-mantra/investment/articles/why-consider-gold-as-an-investment

2. Gold, accessed from: https://www.gold.org/goldhub/gold-focus/2022/01/strategic-case-gold-india

3. ET Money, accessed from: https://www.etmoney.com/learn/mutual-funds/gold-investment-options-in-india-which-one-is-best-for-you/

4. Coverfox, accessed from: https://www.coverfox.com/personal-finance/gold-rate-today/top-gold-saving-schemes-in-india/

5. Clear tax,accessed from: https://cleartax.in/s/sovereign-gold-bonds

6. Cashoverflow, accessed from: https://www.cashoverflow.in/invest-in-gold-india/

7. Bajaj MC, accessed from: https://www.bajajamc.com/knowledge-centre/gold-investment-in-india

8. Bajaj MC, accessed from: https://www.bajajamc.com/knowledge-centre/gold-investment-in-india

9. Piramal Finance, accessed from: https://www.piramalfinance.com/vidya/making-gold-investment-accessible